Balanced Market!

Balanced Market!

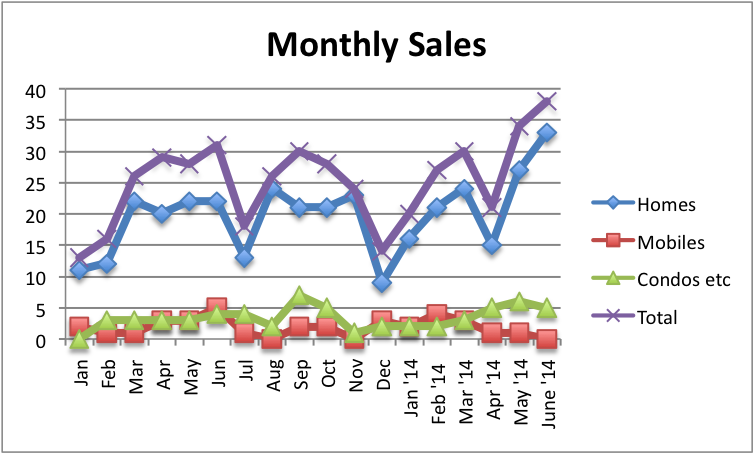

The local real estate market continues to be very active. In May, 34 sales of residential properties (single family, mobiles, condos) was the highest in over a year and a half. The month of June topped that at 38! At the same time, new listings for June jumped to 74, the highest since April 2013. The numbers suggest that we’ve moved from a buyers’ market to a balanced situation which means homes are selling quicker and closer to list price. July and August typically slow down as people turn their attention to holidays and summer fun. We’ll see!

What is CMHC?

History:

The Canadian Mortgage and Housing Corporation was created after WW II to assist with affordable housing and administer the National Housing Act. This is still the mandate. It has grown to oversee lenders, provide mortgage insurance and facilitate Canada Mortgage Bonds and other financial tools to ensure a steady flow of investment into the mortgage market.

For Buyers:

CMHC provides a lot of useful information about the home buying process, financial assistance and mortgages. It’s worth taking a look even if you’re not planning a move (http://www.cmhc.ca). For many buyers, your introduction to CMHC will occur when you talk to your bank about getting a mortgage. If you’re getting a “conventional” mortgage you may not run into CMHC at all. If your downpayment on the property will be less than 20% of the purchase price, then you’re looking for a non-conventional mortgage. Because such a mortgage is deemed to be higher risk for the lender, buyers in this situation are required to get “mortgage default insurance” for which they pay a fee depending on the size of their downpayment. The fees can run from 0.6% up to 3.35% of the amount to be borrowed with the greater charge going for the greater risk (lower downpayment). With mortgage insurance, you can purchase a home with as little as 5% down.

The insurance premium (0.6 to 3.35%) is generally calculated then added to the amount of the mortgage to be paid out over the length of the mortgage and will be subject to the negotiated interest rate on the mortgage. In Canada, approximately 50% of mortgages are insured. The rate of 90 days mortgage arrears in Canada is 0.31% as at August 2013, according to the Canadian Bankers Association. This compares to about 1.26 per cent for prime fixed-rate mortgages in the U.S. for the first quarter of 2013, according to the U.S. Mortgage Bankers Association.

Sub-Prime Lenders…

Even hearing the term, “sub-prime lenders” evokes a nervous reaction in me after the chaos created by the runaway train of sub-prime lending in the USA prior to 2008 (and probably to this day). We had and continue to have sub-prime lenders in Canada too, but as per many other aspects of our financial institutions, ours are subject to more constraints. Sub-prime lenders are those lenders who will lend to people whose credit rating doesn’t meet the standards of the major banks.

There are the 10 basic guidelines you need to know when getting a “B” or sub-prime loan for the purchase of property:

Property needs to be under 4 units

Property can be owner occupied or a rental

Property must be in a marketable urban area

Qualifying ratios are higher making it easier to “fit”

Down payment or equity minimum is 20%

Interest rates will be between 1-3% higher than standard rates

Terms can be as low as 1 year

There are no variable mortgage options only fixed

Current property mortgage cannot be in default with another lender

Mortgage payment history is required for a period of 6-12 months.

B-lenders are not available to the general public so access through a broker is essential.

Staging and Much More…

I wrote about staging homes a couple of months ago. Recently I met Leah Rourke of Powell River’s Relish Interiors. Calling Powell River her hometown, Leah has recently transplanted her business from Victoria to Powell River. She does much more than staging: Interior design and a multitude of other home-decorating related ideas. Check out her website at http://www.relishinteriors.com